Approximately 96 percent of American workers are covered by Social Security, and many more, including non-working spouses, are eligible for payments. In addition, around 40 percent of the average retiree’s income in the United States comes from Social Security.

Thus, for most individuals, deciding when to take Social Security benefits will have a major impact on their ability to live comfortably in retirement.

Do participants have a choice?

A clear and accurate understanding of a participant’s financial situation, both now and in the future, is essential. That understanding can be gained through a thorough review of circumstances and goals.

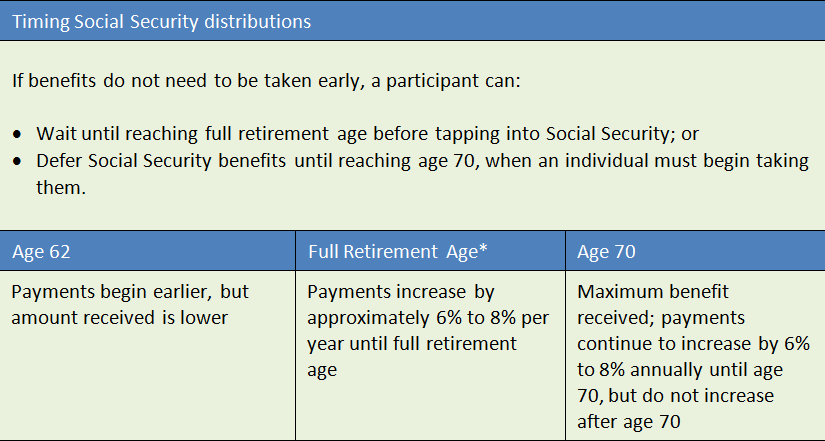

A participant should evaluate whether their core needs and lifestyle spending require collecting monthly Social Security payments as soon as they reach retirement or if the participant can afford to wait until age 70, the point at which benefits are maximized.

More than two-thirds of eligible Americans take their benefits early—after they reach 62, but before they reach full retirement age—often because they simply don’t have a choice: They need the money. However, if a participant does have a choice, not collecting Social Security benefits—even after reaching full retirement age—may make sense.

*To Determine the age at which a participant is qualified for full retirement benefits, visit the Social Security Administration site at ssa.gov.

If health or age is such that a participant is likely to die before their spouse, the participant may want to delay taking benefits as long as possible to increase his or her survivor benefits. In today’s world, those benefits can be an important part of the survivor’s retirement assets, given that couples aged 65 have an 85 percent chance of at least one of them living past 85.¹

Even if a participant delays taking benefits past their full retirement age, their spouse can still take his or her spousal benefits anytime after age 62. During a participant’s lifetime, their spouse is entitled to one-half of the participant’s benefit if it would be greater than what he or she would receive from his or her own earnings.

Please note, changes in tax laws may occur at any time and could have a substantial impact upon each person’s situation. Tax or legal matters should be discussed with the appropriate professional. Source: Society of Actuaries.

This article was originally published in Eagle Asset Management’s retirement brochure, Timing is everything. When to take Social Security. Minor edits were made for compatibility purposes.